What Is IRMAA? How Retirees Can Avoid Higher Medicare Premiums

This morning I was on KTVU Mornings on 2 discussing how many retirees are shocked about how much they are paying in Medicare premiums AKA IRMAA. The key to making sure you don’t pay so much in Medicare premium is to have a plan or strategy so, that you do not have to pay a dollar more than you have too. So, let’s dive into this conversation.

How does Medicare work? When you turn 65 years old you have to apply for Medicare Part A which covers hospital insurance. Part A is generally premium-free. As; it has been pre-paid via payroll taxes. Part B covers doctor visits and outpatient care. While Part D is for prescription drug coverage. Part B and D are not free but are heavily subsidized.

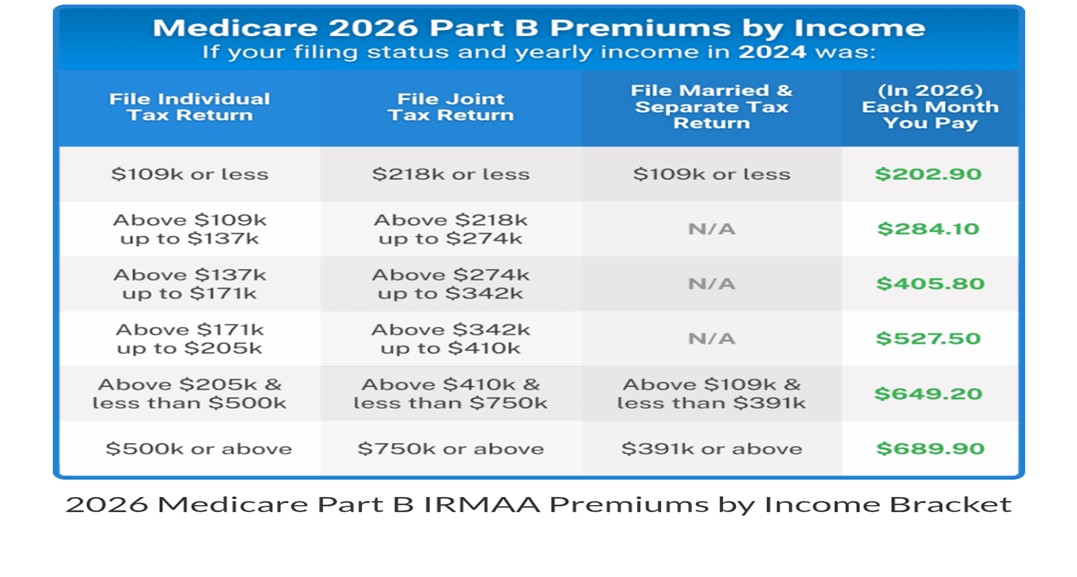

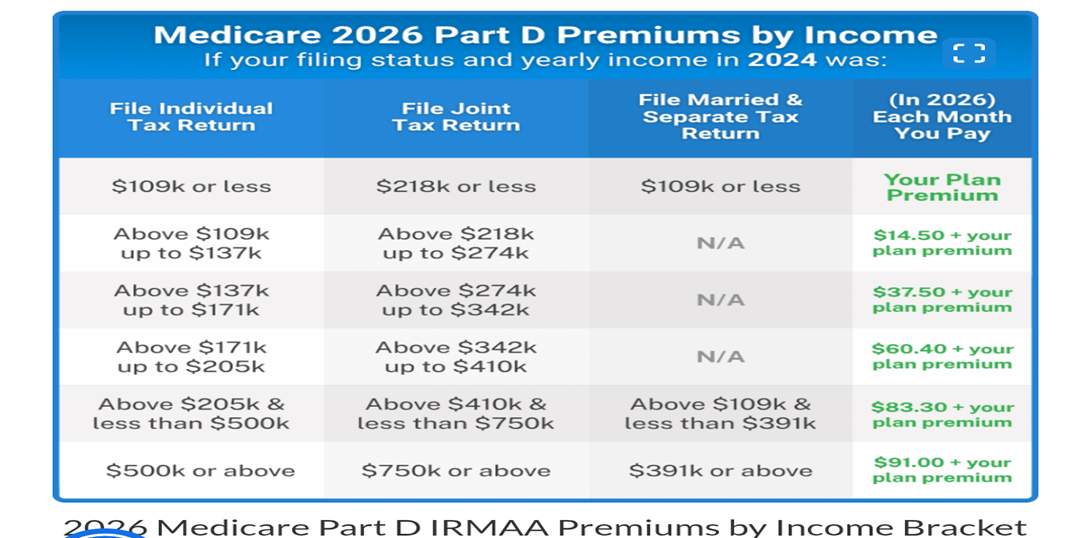

IRMAA which stands for Income-Related Monthly Adjustments Amount. Is a premium AKA a tax on Medicare Part B and D for higher income beneficiaries. You know my belief anytime the government asks you to pay something it is a tax. As; your income increases your subsidy goes away.

IRMAA is based on your income 2 years ago. The problem is many times when we turn 65 we decide to retire. Our IRMAA premiums are based on when we were working at 63 years not 65 when our income is not as high. It can be a huge drain on our finances. This is not a sliding scale, it's a huge cliff. Just $1 over and it can put you in a whole different bracket. That can cause you thousands and thousands of dollars for the year. So, the key is to plan ahead.

Key Planning Considerations

At the age of 63 and older we have to monitor our income levels for our Medicare eligibility. So, we have to be cautious with Roth conversions, IRA withdrawals and capital gains. We should understand the IRMAA threshold as it’s updated annually.

Planning Strategies

Since, IRMAA looks at income at 63 years old 60-62 are prime strategy years.Especially someone in early retirement. You might want to accelerate your income by doing the following:

- Roth IRA conversions

- Capital gains realization

- IRA drawdowns

But make sure since we are accelerating income that we are not putting yourself in a higher tax bracket. This is where you get the help from a professional tax planner to make sure you don't do anything that can hurt you along the way.

Now you might ask what happens if it’s too late? There is exemption that you can do if you have a life changing event such as:

- Marriage

- Divorce or annulment

- Death of spouse

- Work stoppage (retirement)

- A reduction in work

- Loss of income-producing property

- Loss of pension income

- Receipt of any employment settlement package.

If you have any of those life changing events and documentation to support it. Then you can go on the Social Security website and file form SSA-AA requesting a review of your benefits. They can review your application and see if your IRMAA should be adjusted downward.

If you are worried about IRMAA benefits and Medicare and want to look at strategies to reduce your IRMAA premiums and lifetime taxation schedule a retirement check-in.